From Turkey to Tinsel: Why the Holidays Are the Perfect Time to Start Tax Planning

- Mark Toussaint

- Nov 30, 2024

- 3 min read

As the holiday season rolls around, many of us are busy decorating, cooking, and shopping for loved ones. But did you know that this time of year is also ideal for wrapping up your tax planning? The holidays may seem far removed from taxes, but it’s the perfect moment to set yourself up for success in the new year.

Here’s why:

1. Estimated Tax Payments: Avoid a Tax Filing Surprise

The IRS requires many taxpayers to make estimated tax payments throughout the year to avoid penalties. This includes:

Individuals, sole proprietors, partners, and S corporation shareholders: Payments are required if you expect to owe $1,000 or more in taxes when filing your return.

Corporations: Payments are required if you expect to owe $500 or more in taxes when filing.

The final payment for 2024 is due January 15, 2025. Reviewing your income and tax liability now ensures you’re prepared and compliant.

2. Year-End Business Deductions: Make Your Money Work Harder

If you’ve been planning to invest in your business, now’s the time. The IRS allows businesses to deduct up to $1,220,000 in qualified asset purchases made and placed into service by December 31, 2024. This deduction can potentially reduce your taxable income to zero.

What’s even better? You can fund these purchases with loans and still take the deduction. Consider upgrading equipment, investing in technology, or purchasing other assets before the year ends.

3. Tap Into Tax Credits: From Hiring to Energy Savings

Several tax credits are available to reduce your tax bill:

Work Opportunity Tax Credit (WOTC): Hiring workers from specific target groups can earn your business up to $2,400 per qualified employee, or even $9,600 for certain veterans. The WOTC is available through 2025.

Energy Credits: Thanks to the Inflation Reduction Act, businesses can claim credits for installing energy-efficient property or even purchase credits from other sellers. This is a great time to explore green initiatives that benefit your business and the environment.

4. Stay Ahead of Compliance Deadlines

A new requirement in 2024 mandates that most entities, including corporations and LLCs, file a Beneficial Ownership Information (BOI) report. These reports are generally due by December 31, 2024, or earlier for entities formed during the year. Start preparing now to avoid last-minute headaches.

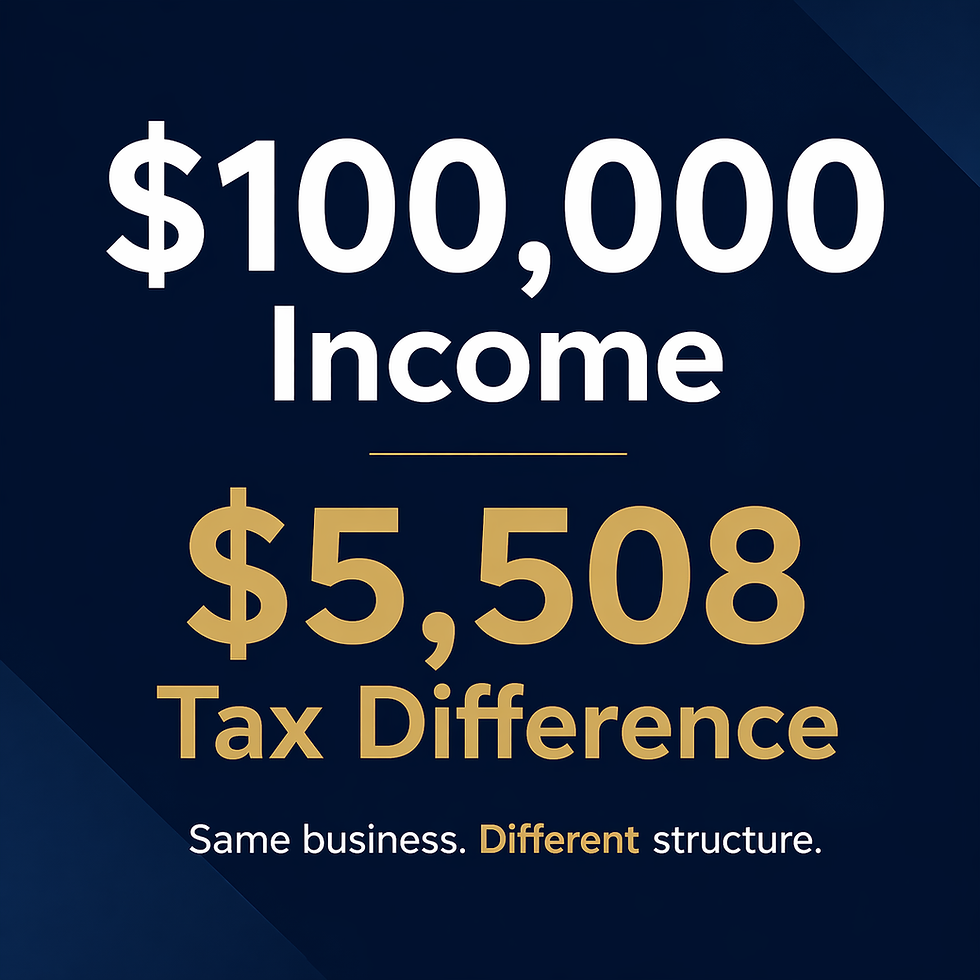

5. Rethink Entity Selection: The Case for C-Corporations

The first of the new year is the ideal time to change your business structure. For many small businesses, switching to a C-corporation can unlock significant tax and financial advantages.

Why Consider a C-Corporation?

Flat 21% Corporate Tax Rate: C-corporations are taxed at a lower rate compared to the individual rates applied to pass-through entities. Max individual rate is 37% + state taxes + Self-employment tax (for partners, SMLLC's and sole proprietors)

Fringe Benefits: C-corporation owners enjoy access to tax-free fringe benefits that S-corporation owners cannot utilize or must treat as taxable income. Here’s how these benefits stack up:

Health Insurance & Medical Reimbursement: Tax-free for C-corporation owners when structured under an HRA or Section 105 plan.

Group-Term Life Insurance: Up to $50,000 in coverage is tax-free for C-corporation owners.

Dependent Care Assistance: Up to $5,000 annually can be provided tax-free.

Education Assistance: Up to $5,250 annually for tuition, books, and fees.

Cafeteria Plans (Section 125): Full pre-tax participation for health and dependent care benefits.

Retirement Plans: Larger contributions with full deductibility for the corporation, not taxed to the owner until distributed.

Planning for the Future: The QBI deduction for pass-through entities is set to expire in 2025. Switching to a C-corporation now may be a forward-thinking move.

Whether you’re looking to maximize owner benefits, reduce personal tax liability, or plan for the phaseout of current deductions, starting the year as a C-corporation could offer substantial advantages.

6. Retirement Plans: A Gift for Your Future Self

Setting up or contributing to a business-sponsored retirement plan before the year ends provides immediate tax savings while helping you prepare for the future. Contributions are tax-deductible for the business, lowering your taxable income for the current year.

Why Now Is the Best Time to Plan

The holidays provide a natural pause to reflect, prepare, and set goals for the new year. By prioritizing tax planning now, you can:

Maximize deductions and credits.

Avoid penalties and surprises.

Position your business for growth and compliance.

So, while you’re decking the halls, don’t forget to deck out your tax strategy. With a little effort now, you can ensure the new year starts with a lower tax bill and a solid financial foundation.

Comments