Unlocking the Potential of the New Child Savings Account

- Mark Toussaint

- Feb 20

- 2 min read

Updated: Mar 8

The Real Opportunity Isn’t Just the Account

Yes, it’s a child savings vehicle. Yes, it grows tax-deferred. And yes — if your child was born between 2025 and 2028, the government will contribute $1,000 to get it started.* But that’s not the interesting part.

The real intrigue lies in how contributions can be made.

What Happens If You Fund It Personally?

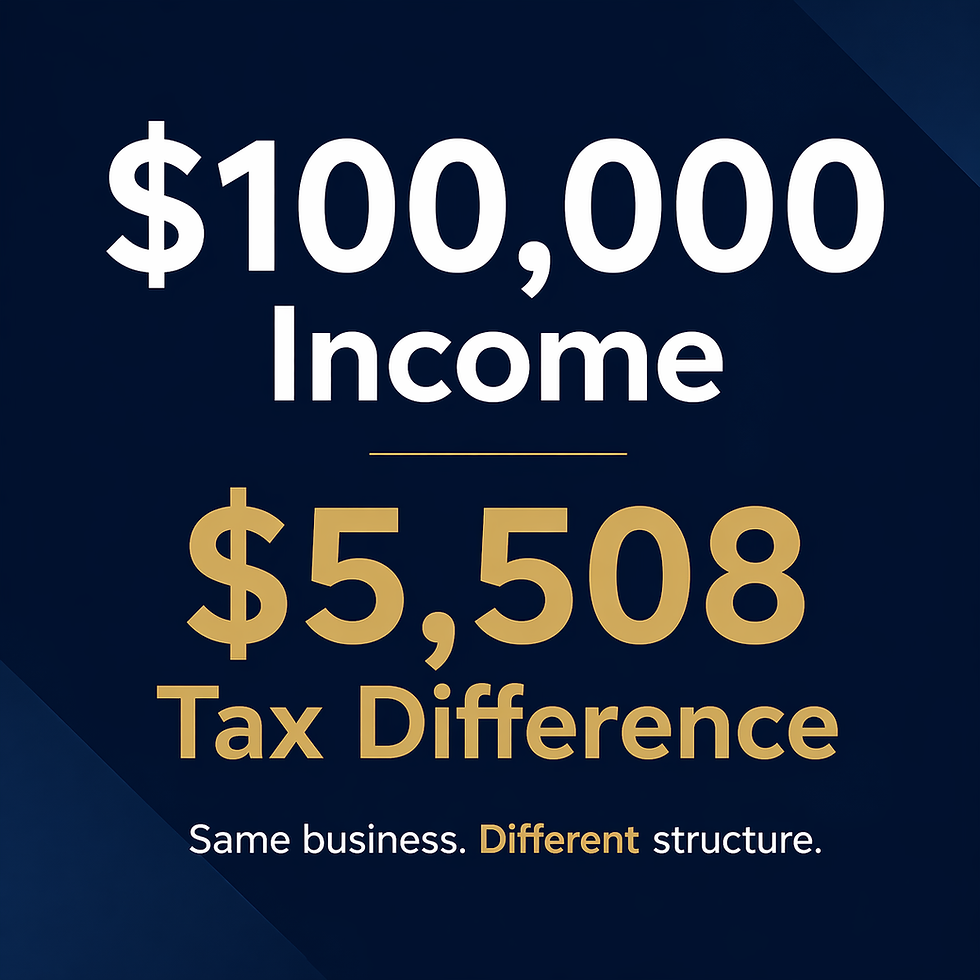

If you pay yourself wages from your business and then contribute personally, you first pay income tax and payroll taxes — and only then invest what remains.

Put differently, a $2,500 contribution made personally can require roughly $4,000–$4,200 in pre-tax business earnings once income and payroll taxes are applied.

That’s the hidden cost most owners don’t calculate.

What Happens If the Business Funds It?

Employers can contribute up to $2,500 per child per year directly. Those contributions are deductible to the business, are not subject to payroll taxes, and are not taxable income to the employee.

So instead of needing over $4,000 in earnings to net $2,500, it simply costs the business $2,500. Same contribution. Very different economics.

That difference is structural — and structural advantages compound over time.

How the Tax Treatment Works (At a High Level)

Contributions are after-tax unless made by the employer. Growth inside the account is tax-deferred, meaning there is no annual tax on dividends or capital gains while the funds remain invested.

There is no forced withdrawal at age 18. Instead, the account transitions into an IRA framework, allowing continued long-term planning and flexibility.

This is not a replacement for a 401(k).

It’s not a replacement for a 529.

It’s another lever.

Effective tax planning is often about stacking the right levers in the right order.

Visualizing the Growth Potential

If you want to visualize how long-term, tax-deferred compounding can grow consistent annual contributions, Fidelity provides an interactive retirement growth calculator:

While designed for retirement accounts, it illustrates how regular contributions in a tax-advantaged structure can accumulate significantly over time.

Is This Strategy Right for You?

Before diving into this strategy, consider your unique financial situation. The child savings account can be a powerful tool, but it’s essential to understand how it fits into your overall financial plan.

Disclaimer: This article is provided for informational purposes only and does not constitute legal, tax, or investment advice. You should consult with a licensed attorney, accountant, or investment advisor before making decisions regarding this or any other financial strategy.

Eligible children born between January 1, 2025, and December 31, 2028, receive a $1,000 federal seed contribution.

Conclusion: Embrace the Opportunity

In conclusion, the new child savings account under the Working Families Tax Cuts Act presents a unique opportunity for business owners. By understanding the nuances of funding this account, you can leverage its benefits to enhance your financial strategy.

Don’t overlook the potential of this tool. Instead, embrace it as a way to secure your child's financial future while optimizing your business's financial health.

By making informed decisions and utilizing the right strategies, you can move beyond messy books and DIY accounting. Achieve financial clarity, make informed decisions, and maximize your earnings through strategic, year-round financial management.

Now, are you ready to explore how this new account can work for you?

Comments